Frequently Asked Questions

Bear River Mutuals’ Most Frequently Asked Questions

Below are some basic questions and answers that might help you answer your questions more quickly. Use the table of contents on the left to more easily navigate to your question!

Bear Care

You can choose any shop for your car repairs! There is no obligation to use a Bear Care provider. We want you to be comfortable with your provider.

But there are benefits to chosing a Bear Care Direct Repair auto body shop:

- Convenience: When you choose a Bear Care Direct shop, you don’t need a third-party appraisal. The required appraisal is pre-approved by Bear River Mutual, and the shop can schedule your repairs promptly. We handle all communication and issues directly, providing you with peace of mind and assurance that your car is in capable hands.

- Peace-of-Mind: Our DRP program shops guarantee their work for as long as you own your vehicle. If you choose a shop outside of our program, we cannot provide the same guarantee.

- Speed: Because of our relationships with these shops, the repair process begins fast, ensuring that you get your vehicle back sooner.

- Quality: We meticulously measure and monitor the work of our DRP shops for many years, and they have our trust and confidence. On average, customers who use a DRP shop report higher satisfaction scores compared to those who do not.

- Efficiency: If additional damage is discovered during the repair process, it won’t cause delays. Our DRP shops are authorized to repair all accident-related damage they find, even beyond the initial estimate.

Finding a trustworthy body shop to fix your car can be difficult and overwhelming. At Bear River Mutual, we want to make your auto insurance claims as easy as possible. We have vetted and selected a group of auto repair shops that meet our high standards for quality and service. These shops are part of our Bear Care Direct Repair Program (DRP), and we guarantee the quality of their work. With us, you can have peace of mind knowing that your car is in good hands.

You can choose any shop for your car repairs but there are benefits to chosing a Bear Care Direct Repair auto body shop:

- Convenience: When you choose a Bear Care Direct shop, you don’t need a third-party appraisal. The required appraisal is pre-approved by Bear River Mutual, and the shop can schedule your repairs promptly. We handle all communication and issues directly, providing you with peace of mind and assurance that your car is in capable hands.

- Peace-of-Mind: Our DRP program shops guarantee their work for as long as you own your vehicle. If you choose a shop outside of our program, we cannot provide the same guarantee.

- Speed: Because of our relationships with these shops, the repair process begins fast, ensuring that you get your vehicle back sooner.

- Quality: We meticulously measure and monitor the work of our DRP shops for many years, and they have our trust and confidence. On average, customers who use a DRP shop report higher satisfaction scores compared to those who do not.

- Efficiency: If additional damage is discovered during the repair process, it won’t cause delays. Our DRP shops are authorized to repair all accident-related damage they find, even beyond the initial estimate.

You can choose any shop for your car repairs but there are benefits to chosing a Bear Care Direct Repair auto body shop:

- Convenience: When you choose a Bear Care Direct shop, you don’t need a third-party appraisal. The required appraisal is pre-approved by Bear River Mutual, and the shop can schedule your repairs promptly. We handle all communication and issues directly, providing you with peace of mind and assurance that your car is in capable hands.

- Peace-of-Mind: Our DRP program shops guarantee their work for as long as you own your vehicle. If you choose a shop outside of our program, we cannot provide the same guarantee.

- Speed: Because of our relationships with these shops, the repair process begins fast, ensuring that you get your vehicle back sooner.

- Quality: We meticulously measure and monitor the work of our DRP shops for many years, and they have our trust and confidence. On average, customers who use a DRP shop report higher satisfaction scores compared to those who do not.

- Efficiency: If additional damage is discovered during the repair process, it won’t cause delays. Our DRP shops are authorized to repair all accident-related damage they find, even beyond the initial estimate.

Car Insurance

First, contact your agent! They are the best resource to make any modifications to your policy.

Make sure you know:

- The driver’s full name

- Date of birth

- Driver’s license number

If it is for a driver that doesn’t live with you (like a child at college), having their temporary address can also be helpful.

If you don’t know who your agent is, you can log in to your customer portal and see their name and contact. Or you can search our full agent listing.

Contact your agent! They are able to help you make any modifications to your policy.

Make sure you have the following information:

- 17- digit Vehicle Identification Number (VIN)

- Date you acquired/sold the vehicle

- Lienholder details if you have a loan

To locate the VIN, look at your bill of sale or registration documents. You can also look at your car itself. Go outside of your car and look through the windshield on the driver’s side. The VIN will be on the bottom corner of the driver’s side dashboard. I can also be on your driver side inside the vehicle. Open the driver door and find a sticker inside the vehicle on the base. In many cases there are barcodes and other manufacturer information, along with the VIN.

If your car is new, your existing policy typically provides up to 14-days of coverage for a new vehicle. It is recommended to add the new vehicle as soon as possible. You do not want to incur any coverage lapse. Waiting does not provide any advantages. Utah insurance laws require coverage to be backdated to when the vehicle was acquired.

Your agent is listed with your other policy information on your customer portal.

Your proof of insurance card, or insurance ID card, can be found in your customer portal. Log in, and you will have a printable format. You can also keep a digital copy on your phone.

Bear River Mutual uses independent agents to sell our policies. Independent agents are licensed professionals able to sell insurance policies for many different insurance carriers. This offers flexibility for you as a customer to find the best policy for you and your needs.

Fill out our online form, and based on your zip code, the agent closest to you will reach out!

If you would like to reduce your premium (the amount you pay for insurance coverage), check with your agent to find out what discounts you may be eligible for.

Discounts may include:

- Claim-Free Discount (no claims filed)

- Policy bundles (home and auto)

Your agent can offer advice and assistance to find the best options for ou to lower costs, while still maintaining coverage.

Your agent’s information can be found in your customer portal.

A deductible is the amount that you need to pay when you experience a covered loss. Bear River Mutual then covers the remaining expenses up to the applicable limit(s) as stated in your policy.

Example:

You have covered expenses that are $2,500. You have a $1,000 deductible. You will be responsible for paying $1,000, and Bear River Mutual will cover the remaining $1,500.

At Bear River Mutual, deductibles apply to comprehensive and collision coverage in our automobile insurance policies.

- Comprehensive coverage: This coverage protects against events that are mostly beyond your control, like a stolen vehicle or a tree falling on your car.

- Collision coverage: This coverage protects you towards incidents that typically result from driver error, even if it’s the fault of the other driver.

If you are not at fault, you have the option to file a claim through the at-fault driver’s insurance company, or file through your policy at Bear River Mutual.

If you file through your policy at Bear River Mutual, you will be responsible for your deductible payment upfront. This can speed up repairs or other processes. We will then attempt to recover and reimburse your deductible amount by the at-fault driver insurance, but that can sometimes be a lengthy process. Or you can wait for the at-fault insurance company to work with you on the claim.

Ask these questions:

- What type of car do you have?

- How many people do you expect to have in it?

- What is your financial situation?

A Bear River Mutual independent agent can help you find the best coverage options that meet your specific needs!

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

No! In the state Utah it is a legal requirement to maintain no-fault (aka liability) insurance on all passenger cars and trucks for the entire registration period. The Utah State Legislature has established minimum liability limits that insurance companies operating in the state must adhere to for motor vehicle insurance policies. As a vehicle owner in Utah, it is your responsibility to be insured for any vehicle you drive.

Insurance companies have a part to play, too! They must provide coverage that meets or exceeds the mandatory minimum limits imposed by the state.

Driving without insurance is considered a Class B misdemeanor. This can result in license suspension, vehicle registration suspension, and hefty fines from the state or a lienholder.

Consult with an agent to understand the specific coverage limits and obligations that would apply to you.

References: Utah Division of Motor Vehicles, Vehicle Insurance Requirements | Utah State Legislature, 31A-22-304, Motor vehicle liability policy minimum limits.

First, you must see if you have comprehensive coverage on your policy. If your vehicle has comprehensive coverage, you may be eligible for coverage for minor repairs (rock chips, etc.) at no additional cost. A full windshield replacement, however, is subject to the deductible specified on your policy for that vehicle. You may also have an added line in your policy that says “(Glass only).” This gives a specific deductible for glass replacement. This is something that you can choose to add when you instate your policy, but it is not standard. Also note, a sunroof/moonroof is not a part of the general Glass Only endorsement.

")

Bear River partners with Safelite for all glass repairs (🎶Safelite repair, Safelite replace🎶). If you use Safelite, they work with us directly for billing and payment. The costs of materials and labor are discounted, and any windshield work is guaranteed for 30 days. They are able to re-calibrate windshields for nearly any vehicle.

You may use another provider. However, they will require payment from you directly. Receipts and workorders can be sent for reimbursement. There are limits to minor repair payment, and any work done would not be guaranteed by Bear River.

CONTACT SAFELITE:

Call or click!

(801) 267-5001 or (800) 925-5177, option 3.

Want to add Glass coverage to your policy? Contact your agent!

Your agent is listed with your other policy information on your customer portal.

Still have questions? Call our service line.

Customer Service:

(801) 267-5000

This is a personal decision. It can depend on your preferences and financial approach, and every customer may view these differently.

A higher deductible results in lower premiums (your monthly cost). However, if you file a claim, you will pay more out-of-pocket. A lower deductible will lead to a higher premium, but you will pay less for filing a claim.

Contact your agent to help you understand your options, and what would work best for you.

Log into the customer portal to see your agent’s contact information.

You may consider opting out of comprehensive coverage if:

- Your car is older and fully paid for

- You are not concerned about minor cosmetic damage

- Your car is at the end of its lifespan

- Your car has a low market value

Coverage amounts are based on the current market value of your vehicle, and any claims are subject to your deductible.

Call your agent to discuss what would work best for you.

Your agent’s contact information can be found by logging in to your customer portal.

To process a complete and accurate quote, an independent agent will need the following information:

- Name and date of birth for each driver included in the policy

- Vehicle Identification Number (VIN) for all vehicles to be covered under the policy

- Driver’s licence number for each covered driver

- Driving history for each covered driver

- Name of the leinholder for any vehicles that have a loan

- Existing damage to the covered vehicle

- Addresses for all drivers covered (ex: a dependant child covered on the policy is away at college)

Your auto insurance policy typically extends coverage to you, your spouse/partner, relatives residing in your household, and other licensed drivers who have your permission to drive your insured vehicle. The specific details outlined in your policy dictate the exact coverage and exclusions.

If you have any questions about your coverage, reach out to your agent.

Your agent’s contact information can be found by logging in to your customer portal.

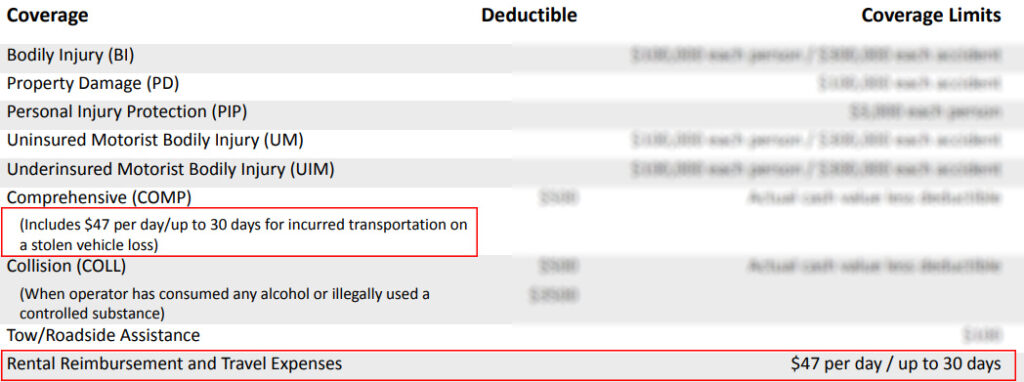

Rental coverage is an optional addition to your insurance policy. It is vehicle-specific coverage that can be added upon request. To check if you have rental coverage, view your policy information.

If rental coverage is included on your vehicle, you will find specific information on your policy document, known as the “AUTOMOBILE INSURANCE DECLARATIONS PAGE.” This will outline the maximum rental charges allowed per day, up to a maximum of 30 days per covered claim. The rental days covered do not need to be consecutive. The amount of coverage can vary and depends on what you selected when you instated your policy.

If you are still unsure of your rental coverage, contact your agent. They can help you understand your policy, or add rental coverage for future claims.

When you receive a rental car for your claim, the rental will end when the repairs to your vehicle have been completed, when you receive a total loss offer, or when you’ve had the rental for 30 days, whichever comes first. All Enterprise requires a $50.00 refundable deposit, valid driver’s license, and proof of insurance.

If you have filed a claim, have rental coverage, and are ready to get in a rental vehicle, call our customer service line and a representative can help you.

Customer Service:

(801) 267-5000

Liability coverage protects you in case of injury or damage to others. Here is an overview of the different types of liability coverage:

- Bodily Injury Liability: This coverage helps pay for medical expenses of the injured party. It also offers legal protection in case of a lawsuit, up to the limit stated in your policy.

- Property Damage Liability: If you damage someone else’s property, such as their car or mailbox, this coverage helps cover the costs of repairs or replacements, up to the limit stated in your policy.

- Personal Injury Protection (PIP): PIP coverage assists in covering medical expenses and related costs if you or your passengers are injured in an accident. Even if you are not at fault, you may need to open a claim with us for medical expenses covered by your PIP coverage.

- Uninsured/Underinsured Motorist: This coverage protects you if you’re in an accident with a driver who doesn’t have insurance or has insufficient coverage to pay for the damages.

- Collision Coverage: If your vehicle is damaged in a collision with another vehicle or object, collision coverage helps pay for repairs or replacement.

- Comprehensive Coverage: This coverage pays for the repair or replacement of your vehicle if it’s damaged by something other than a collision, such as theft or vandalism.

It is important to note that the coverage limit sets a maximum amount that can be paid, but it does not guarantee full payment in every situation. It is crucial to review and select coverage limits that align with your needs and potential risks.

Discuss your coverage with your agent to decide what works best for your needs.

Your agent’s contact information can be found by logging in to your customer portal.

Claims – Auto

With a Bear River Mutual Policy, you are covered in all US states, territories, and Canada!

File your claim, and your adjuster will guide you through the process, and answer any questions you may have.

A total loss is when the cost of fixing your car is more than the fair market value of your car. Trained appraisers inspect your vehicle to determine the fair market value.

Bear River Mutual will provide payment for the cash value of the loss, minus the deductible, and minus any outstanding loan on the vehicle.

For example:

Car value = $6,000

Deductible = $1,000, you pay

Outstanding loan = $3,500, Bear River settles with Lienholder

You receive $1,500.

If the outstanding loan balance is more than the value, you will be responsible for settling that amount with your creditor.

A total loss is when the cost of fixing your car is more than the fair market value of your car. Trained appraisers inspect your vehicle to determine the fair market value.

Once an agreement is made on the vehicle valuation, you will sign over the title to Bear River Mutual. Payment will be made to you, or to leinholder, if there is an outstanding loan balance.

If rental coverage is included on your vehicle, you will find specific information on your policy document, known as the “AUTOMOBILE INSURANCE DECLARATIONS PAGE.” This will outline the maximum rental charges allowed per day, up to a maximum of 30 days per covered claim. The rental days covered do not need to be consecutive. The amount of coverage can vary and depends on what you selected when you instated your policy.

If you are still unsure of your rental coverage, contact your agent. They can help you understand your policy, or add rental coverage for future claims.

When you receive a rental car for your claim, the rental will end when the repairs to your vehicle have been completed, when you receive a total loss offer, or when you’ve had the rental for 30 days, whichever comes first. All Enterprise requires a $50.00 refundable deposit, valid driver’s license, and proof of insurance.

If you have filed a claim, have rental coverage, and are ready to get in a rental vehicle, call our customer service line and a representative can help you.

Customer Service:

(801) 267-5000

First, take a deep breath! We will help you manage the claims process.

As a Bear River Mutual policyholder, initiate the claims process online. You can also contact your agent, or call our service line to speak with one of our team members.

We will ask you questions to gather information about the accident. We will also ask for policy information and contact information for everyone involved.

Once a claim is filed, a claim representative will reach out to guide you, answer questions, and give support and assistance.

Customer Service:

(801) 267-5000

Filing a claim is a straightforward process. You have three options to initiate the claims process:

- Online: You can begin the claims process online.

FILE A CLAIM ONLINE:

- Contact your agent: Your agent can start the claims process for you. One of our representatives will then reach out to go over any additional questions that you may have, and possibly ask you to provide additional information that can help the claims process proceed more smoothly.

To contact your agent, you will see their contact information listed in your policy information on the customer portal.

- Call Bear River Mutual: A customer service representative will guide you through the claims process and address any questions or concerns you may have.

CALL TO FILE

(801) 267-5001

(800) 925-5177, option 3

Be ready to provide basic details about the nature of the loss, including the date of the incident, what happened, who was involved, and what damage was incurred.

Claims – General

The time it takes to get your payment depends on the specifics of your claim. However, in most cases, once an agreed-upon cost or settlement has been reached, the payment process is completed quickly.

Yes, your deductible always applies, even if you are not at fault. However, if the other party accepts liability, their insurance will cover the cost of your damages including your deductible.

You have the option to file a claim through the at-fault driver’s insurance company, or file through your policy at Bear River Mutual.

If you file through your policy at Bear River Mutual, you will be responsible for your deductible payment upfront. This can speed up repairs or other processes. We will then attempt to recover and reimburse your deductible amount by the at-fault driver insurance, but that can sometimes be a lengthy process.

Or you can wait for the at-fault insurance company to work with you on the claim.

If you have concerns regarding your settlement amount, communicate with your claims adjuster. They are there to listen, and work with you, to reach a fair and accurate estimate.

They can explain the process and methodology of the settlement offer, and the experts involved. We want you to be satisfied and value your input throughout the claims process.

The required timeframe for filing a claim varies depending on the type of policy you have and the nature of the claim. Review your policy documents to understand the specific timelines for filing a claim.

We recommend filing soon as possible following the incident to report your claim and discuss next steps. The earlier you initiate the claims process, the faster the resolution.

If you find yourself facing a lawsuit from the other party involved in the incident, contact your claims adjuster immediately.

There are specific deadlines for responding to a filed suit. Your adjuster is an experienced professionals who can guide you through the necessary steps and provide you with advice on how to proceed.

Filing a claim is a straightforward process. You have three options to initiate the claims process:

- Online: You can begin the claims process online.

FILE A CLAIM ONLINE:

- Contact your agent: Your agent can start the claims process for you. One of our representatives will then reach out to go over any additional questions that you may have, and possibly ask you to provide additional information that can help the claims process proceed more smoothly.

To contact your agent, you will see their contact information listed in your policy information on the customer portal.

- Call Bear River Mutual: A customer service representative will guide you through the claims process and address any questions or concerns you may have.

CALL TO FILE

(801) 267-5001

(800) 925-5177, option 3

Be ready to provide basic details about the nature of the loss, including the date of the incident, what happened, who was involved, and what damage was incurred.

Claims – Home

The decision of which contractor to use for your home repairs is entirely up to you. We want you to feel comfortable and confident in your choice, so you should never feel pressured to select a contractor that you are not comfortable with. While we highly recommend using a Bear Care Home Repair Program contractor due to the numerous benefits they offer, ultimately, the choice is yours. We believe in providing you with options and ensuring that you have the flexibility to choose the contractor that best suits your needs and preferences.

We understand that finding a reliable contractor to repair your home can be overwhelming. That’s why we have developed the Bear Care Home Repair program to simplify the process for you. This program provides access to a network of contractors who have been carefully vetted by Bear River Mutual to ensure they deliver exceptional service and repairs. These trusted contractors are part of our exclusive Bear Care Home Repair Program, and we stand behind their work with our guarantee. With this program, we aim to alleviate the uncertainty and stress often associated with home insurance claims, providing you with peace of mind and reliable assistance throughout the repair process.

Filing a claim is a straightforward process. You have three options to initiate the claims process:

- Online: You can begin the claims process online.

FILE A CLAIM ONLINE:

- Contact your agent: Your agent can start the claims process for you. One of our representatives will then reach out to go over any additional questions that you may have, and possibly ask you to provide additional information that can help the claims process proceed more smoothly.

To contact your agent, you will see their contact information listed in your policy information on the customer portal.

- Call Bear River Mutual: A customer service representative will guide you through the claims process and address any questions or concerns you may have.

CALL TO FILE

(801) 267-5001

(800) 925-5177, option 3

Be ready to provide basic details about the nature of the loss, including the date of the incident, what happened, who was involved, and what damage was incurred.

- Convenience: With a Bear Care Home Repair contractor, there’s no need for a separate appraisal process. When our approved contractor assesses the damage, the appraisal is pre-approved by Bear River Mutual, saving you time and hassle. They can schedule your repairs, and we handle all communication and issues directly with them. Rest assured that your home is in capable hands.

- Peace of Mind: Our Bear Care Home Repair program guarantees the work of our contractors for three years. If you choose your own contractor, we cannot guarantee their work. By opting for a Bear Care contractor, you can have confidence in the quality and reliability of the repairs.

- Speed: Our established relationships with these contractors facilitate quick communication and expedite the repair process. You can expect your home to be restored to its original state in a timely manner.

- Quality: We have closely monitored the work of our Bear Care Home contractors for many years, and they have earned our utmost trust and confidence. Customers who choose our preferred contractors consistently report higher satisfaction scores compared to those who do not.

- Efficiency: If additional damage is discovered during the repair process, it won’t cause delays in your repairs. Our Bear Care Home contractors are authorized to address all claim-related damage they encounter, even if it goes beyond the initial estimate. This ensures a comprehensive and efficient restoration of your home.

By utilizing a Bear Care Home Repair contractor, you can enjoy the convenience, peace of mind, speed, quality, and efficiency that come with our trusted network of professionals.

If your home has been damaged, we recommend taking the following steps:

- Ensure Safety: Prioritize the safety of yourself and your family. If there are any immediate hazards, such as structural damage or electrical issues, evacuate the premises and seek assistance if needed.

- Consult Your Independent Agent: Your agent can give advice and guidance as you begin your claim. They can help you determine if filing a claim is the right course of action for your situation.

- Mitigate Further Damage: Providing you can do so safely, take necessary measures to prevent additional damage to your home. This may include things like covering exposed areas with tarps or boards, shutting off the water supply, or turning off the electricity.

- Document the Damage: When it’s safe, document the damage by taking pictures or video. This evidence will be valuable when filing your insurance claim.

- Contact Us: After ensuring safety and mitigating further damage, you can begin the claims process.

FILE ONLINE:

CALL TO FILE

(801) 267-5001

(800) 925-5177, option 3

Earthquake Insurance

No, Bear River Mutual does not offer earthquake coverage.

Your independent agent can help you in obtaining this type of coverage for your property from another provider.

Earthquake insurance provides coverage in the event that your home is damaged by an earthquake. A standard homeowner policy does not cover earthquake damage.

Earthquake insurance may cover various aspects, including:

- Repairs to Your Home

- Personal Property

- Debris Removal

- Additional Living Expenses if your home becomes uninhabitable.

General

We understand that circumstances may arise where you need to cancel your Bear River Mutual policy. While we’re sorry to see you go, we want to make the cancellation process as smooth as possible for you. Here’s what you need to do:

- Contact Your Agent: To initiate the cancellation of your policy, simply reach out to your independent Bear River Mutual agent. They will assist you in the cancellation process and take care of the necessary steps on your behalf.

By contacting your agent directly, you can ensure that all the required paperwork and procedures are handled correctly. They will guide you through the process, answer any questions you may have, and address any concerns that arise during the cancellation.

We appreciate your time as a policyholder and value your feedback. If there are any specific reasons for your cancellation, we would appreciate hearing from you so that we can continually improve our services.

Bear River Mutual has received an AM Best Rating of A- (Excellent). AM Best is the largest credit rating agency globally, specializing in evaluating the financial strength and stability of insurance companies.

The AM Best Rating is significant because it provides an objective assessment of an insurer’s ability to fulfill its obligations to policyholders. A higher rating indicates a stronger financial position and a greater likelihood of meeting claims and other policyholder needs.

Bear River Mutual’s A- (Excellent) rating reflects our commitment to financial stability and our ability to provide reliable coverage and service to our policyholders.

To stay up-to-date with the latest Best’s Credit Rating for Bear River Mutual, you can visit the AM Best website at www.ambest.com.

We believe that our AM Best Rating is a testament to our dedication to serving our policyholders and providing them with the peace of mind they deserve.

No, Bear River Mutual does not offer earthquake coverage.

Your independent agent can help you in obtaining this type of coverage for your property from another provider.

Earthquake insurance provides coverage in the event that your home is damaged by an earthquake. A standard homeowner policy does not cover earthquake damage.

Earthquake insurance may cover various aspects, including:

- Repairs to Your Home

- Personal Property

- Debris Removal

- Additional Living Expenses if your home becomes uninhabitable.

Home Insurance

You can modify and adjust your coverage at any time. If you are making improvements to your home, such as adding an extension, finishing your basement, or upgrading any other part of your property, you want to ensure that your coverage aligns with the new value of your home.

To make changes to your coverage amount, simply reach out to your agent.

You will see your agent’s contact information listed in your policy information on the customer portal.

Yes, Bear River Mutual offers Buried Utility Line coverage. This is also known as Service Line coverage. It is an optional addition to our homeowners policies. This endorsement provides coverage for various items, including:

- Underground piping: This includes water, sewage, and gas lines that are buried beneath the ground.

- Buried connections, valves, or equipment: Any underground components that are connected to or serve the underground piping

- Underground wires: Coverage extends to electrical cables, power lines, and communication or data wiring that are buried underground.

To learn more about the specific details of our Buried Utility Line coverage HERE.

You can also reach out to your agent. They can provide you with comprehensive information about this coverage and other insurance options available from Bear River Mutual.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

If you are considering a new policy, and would like to find an agent you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Yes, Bear River Mutual offers Equipment Breakdown coverage as an optional addition to our homeowner’s policies. This endorsement provides coverage for a wide range of items, including kitchen appliances, home entertainment equipment, and air-conditioning systems.

Learn more about equipment breakdown coverage HERE.

You can also contact your agent to discuss if this coverage is something you need on your policy.

To contact your agent, you will see their contact information listed in your policy information on the customer portal.

No. A lender, realtor, or other party may offer recommendations, but they cannot make the choice for you.

We encourage you to thoroughly research and compare different insurance carriers to find the one that offers the best coverage, service, and value for your individual circumstances.

A Bear River Mutual independent agent can help you find the best coverage options that meet your specific needs!

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

To receive a quote for homeowners insurance from Bear River Mutual, reach out to one of our independent agents. They are authorized to quote and sell Bear River Mutual insurance policies.

Finding an agent in your area is simple. By clicking on our agent search tool, you can easily locate an agency that represents Bear River Mutual near you. Our network of independent agents is dedicated to providing personalized service and helping you find the right coverage for your home.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

You can also fill out our online form to get a quote, and an agent will get back to you!

The amount of homeowners insurance coverage you require depends on various factors. Primarily, your coverage should be sufficient to cover the cost of rebuilding your home and replacing all your possessions in the event of a catastrophic event.

Calculating the appropriate coverage amount involves considering factors such as the size, construction, and features of your home, as well as the current costs of labor and materials in your area. It is essential to evaluate the replacement value of your home, rather than its market value.

Additionally, you should assess the value of your personal belongings, including furniture, appliances, electronics, and other possessions. Creating a comprehensive home inventory list can be helpful in determining the total value of your belongings.

At Bear River Mutual, we recommend consulting with one of our trusted independent agents to assist you in determining the appropriate coverage amount for your specific circumstances. They have the expertise to guide you through the process and ensure that you have the right level of protection for your home and possessions.

Remember, having adequate homeowners insurance coverage provides you with the peace of mind that comes from knowing you are financially protected in the face of unforeseen events.

A home inventory list is a record that includes details like photographs and receipts of items within your home. These can be helpful during a claim. It helps to accurately assess the value of your personal property and posessions. This list can also help ensure that you have the right protection for your belongings.

A home inventory list is not mandatory. But it can be helpful when determining the appropriate coverage levels for your insurance policy.

Certain high-value items, such as jewelry or firearms, may have specific coverage limits. If you own unique or high-value personal property, discuss additional coverage options with your agent. They can provide guidance on how to protect these items adequately.

You will see your agent’s contact information listed in your policy information on the customer portal.

Homeowners insurance covers repairs or replacements to your home’s structure and belongings. It also offers protection if you are found liable for injuries to others or damage to their property.

Standard home insurance policies are designed to safeguard you against specific types of damage. These typically include events like fire, theft, vandalism, and certain natural disasters. However, coverage can vary depending on the specific policy.

Work with your independent Bear River Mutual agent to find the coverage that best suits your needs. They can answer any questions you may have about homeowners’ insurance, help you assess the risks you face, and recommend appropriate coverage options to ensure you have the protection you need.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Renters Insurance

Renters insurance policies only provide coverage for items owned by the policyholder. This means that your roommates’ belongings are not covered under your policy.

Each individual residing in your rental property should consider obtaining their own renters insurance policy to protect their personal belongings. This ensures that everyone has coverage tailored to their specific needs.

.

To receive a quote for Renters Insurance from Bear River Mutual, we recommend reaching out to one of our trusted independent agents. These agents are authorized to quote and sell Bear River Mutual Insurance policies, including Renters Insurance.

Obtaining a quote is simple. You can connect with any agency that represents Bear River Mutual to request a quote for Renters Insurance. Our network of independent agents is dedicated to providing personalized service and helping you find the right coverage for your rental property.

When you contact a Bear River Mutual agent, they will guide you through the quoting process, taking into account your specific needs and preferences. They will gather the necessary information to provide you with an accurate and tailored Renters Insurance quote.

At Bear River Mutual, we understand the importance of protecting your personal belongings and liability as a renter. We encourage you to take advantage of our independent agents’ expertise and reach out to them for a Renters Insurance quote that meets your requirements.

By working with a Bear River Mutual agent, you can have confidence that your rental property is adequately protected, giving you peace of mind knowing you are financially safeguarded in case of unforeseen events.

Filing a Renters Insurance claim is a straightforward process. You have three options to initiate the claims process:

- Online: You can begin the claims process online.

FILE A CLAIM ONLINE:

- Contact your agent: Your agent can start the claims process for you. One of our representatives will then reach out to go over any additional questions that you may have, and possibly ask you to provide additional information that can help the claims process proceed more smoothly.

To contact your agent, you will see their contact information listed in your policy information on the customer portal.

- Call Bear River Mutual: A customer service representative will guide you through the claims process and address any questions or concerns you may have.

CALL TO FILE

(801) 267-5001

(800) 925-5177, option 3

The cost of renters insurance premiums can vary and is determined by coverage limits, deductibles, and the location of your rental property.

To get an accurate price quote based on your specific needs and situation, reach out to your independent agent. They can guide you to choose the right coverage based on your belongings, the level of coverage you want, and any other coverage options that may be applicable.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Renters liability insurance is designed to protect you in case you are found liable for damages caused by negligence. For example, if you accidentally leave the kitchen sink on and it overflows, causing damage to your neighbors’ apartment, you could be held responsible for the resulting expenses. This may include repairs, medical bills, and even legal defense costs if your neighbors decide to take legal action against you.

While renters liability insurance covers these specific costs, it is important to note that it does not provide coverage for other essential aspects of renters insurance, such as personal property, living expenses, and other important coverages.

Liability insurance alone may not satisfy all the coverage requirements set by your landlord. They may also require you to have additional coverage for your personal belongings and other potential risks.

To ensure you meet your landlord’s requirements and have comprehensive protection, it is recommended to have a renters insurance policy that includes liability coverage along with coverage for personal property, living expenses, and other essential aspects.

Work with an independent agent to obtain a renters insurance policy that will meet your specific needs, including any requirements set by your landlord. They can help you understand the coverage options available and assist you in selecting the right policy that provides the necessary protection.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Renters, or “tenants,” insurance, is for those who rent their living space, whether it’s an apartment, condo, or house. Renters insurance is similar to homeowners insurance, with a few key differences. Homeowners insurance covers both the items within the dwelling and its structure. Renters insurance provides coverage for the belongings and liability of the renter, but not coverage for the actual building or structure. It offers financial protection in case of unforeseen events, such as theft, fire, or damage to personal property. This includes coverage for items like furniture, electronics, clothing, and other belongings that you own.

A comprehensive renters insurance policy can include:

- Liability Coverage: This protects you if someone is injured on your rental property and holds you responsible for the incident. It can help cover medical expenses, legal fees, and other costs associated with liability claims.

- Personal Belongings Protection: Renters insurance safeguards your belongings in case of damage or theft. This includes coverage for things like electronics, furniture, clothing, and other personal possessions. If your belongings are damaged or stolen, renters insurance can help cover the cost of repairing or replacing them.

- Additional Living Expenses: If your rented home becomes temporarily uninhabitable due to a covered event, renters insurance can help cover the costs of alternative accommodations, like hotel stays or temporary rentals.

- Medical Expenses: This coverage can help pay for medical bills and related expenses if someone is injured on your rented property.

To learn more about renters insurance, talk to a Bear River Mutual agent!

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

It is crucial to have renters insurance because the insurance typically provided by apartment complexes and landlords only covers damage to the physical structure of the dwelling itself. This means that your personal belongings, such as electronics, furniture, and clothing, remain vulnerable and unprotected.

To safeguard your possessions in the event of unforeseen circumstances like fire, theft, or damage, it is essential to have your own insurance policy known as an HO4 or renters insurance policy.

Renters insurance offers comprehensive coverage for your personal belongings, providing financial protection in case of unexpected events. If your belongings are damaged or stolen, renters insurance can help cover the cost of replacing or repairing them, ensuring that you are not left with a significant financial burden.

Additionally, renters insurance often includes liability coverage, which protects you if someone is injured at your residence and holds you responsible. This coverage can help cover medical expenses, legal fees, and other costs associated with liability claims.

By obtaining renters insurance, you can have peace of mind knowing that your belongings are protected and that you have coverage in place to handle potential liability issues. It is a wise investment that safeguards your financial well-being and provides security for your personal belongings.

Umbrella Insurance

To add umbrella insurance coverage to your current policy, there are a few requirements to consider. You must have both Home and Auto policies with Bear River Mutual, and these policies need to meet specific coverage levels.

If you meet these criteria and would like to add umbrella insurance to your coverage, simply reach out to your dedicated Bear River Mutual agent. They will assist you in the process of adding umbrella insurance to your policy.

Contacting your agent is the best way to request any additions or modifications to your policy. They have the knowledge and expertise to guide you through the necessary steps and ensure that your coverage is tailored to your specific needs.

Don’t hesitate to get in touch with your Bear River Mutual agent to discuss supplementing your existing coverage with an umbrella policy. They are here to provide you with personalized assistance and help you secure the additional protection you desire.

Bear River Mutual provides umbrella coverage limits of $1,000,000 and $2,000,000. To make any changes to your policy and request an increase in coverage, simply get in touch with your Bear River Mutual agent.

You will see your agent contact information listed in your policy detail on the customer portal.

To get a quote for umbrella insurance from Bear River Mutual, reach out to one of our independent agents. They are authorized to quote and sell Bear River Mutual insurance policies.

Finding an agent in your area is simple. By clicking on our agent search tool, you can easily locate an agency that represents Bear River Mutual near you. Our network of independent agents is dedicated to providing personalized service and helping you find the right coverage for your home.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

You can also fill out our online form to get a quote, and an agent will get back to you!

To understand the amount of umbrella insurance coverage you need, you must consider the assets you need to protect. Evaluate your specific circumstances and the potential risks you may face. Consider factors such as the value of your assets, including your home, vehicles, investments, and savings. Also, take into account your potential liability risks, such as the likelihood of being involved in a lawsuit or facing significant financial claims.

Bear River Mutual offers umbrella coverage limits of $1,000,000 and $2,000,000 to provide flexibility in choosing the appropriate coverage level for your needs.

Work with your independent Bear River Mutual agent to find the coverage that best suits your needs. They can answer any questions you may have, help you assess the risks you face, and recommend appropriate coverage options to ensure you have the protection you need.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Umbrella insurance provides additional protection for your assets. It serves as excess liability insurance, extending beyond the limits of your home, auto, or other liability policies.

If you are held responsible for damages or face a significant liability claim, umbrella insurance steps in to provide coverage beyond what your primary policies offer. It acts as a safeguard to protect your assets from potential financial burdens resulting from lawsuits or substantial claims.

Bear River Mutual provides umbrella policy limits of $1,000,000 and $2,000,000.

Example:

Let’s say you are involved in an automobile accident and are sued for $1,000,000 in damages. If your auto policy has a liability limit of $500,000, your umbrella policy would then come into play to cover the remaining $500,000.

Umbrella insurance acts as an additional layer of protection, filling the gap between the limits of your primary policies and the total amount of damages or claims you may face. It provides coverage for various liability situations, such as bodily injury, property damage, defamation, and more.

An umbrella policy can create peace of mind knowing that you have extra coverage to help safeguard your assets and protect you from potentially significant financial burdens resulting from lawsuits or serious claims.

If you have more questions, reach out to a Bear River Mutual Independent agent. They can help you understand if Umbrella Inurance is right for you and your circumstances.

If you already have an agent, you will see their contact information listed in your policy information on the customer portal.

To find an agent, you can use our search page. Simply enter in your zip code to find the independent agent closest to you!

Umbrella insurance provides additional coverage that can help safeguard your assets in the event of lawsuits and significant claims. It offers an extra layer of protection beyond the limits of your primary insurance policies.

There are several reasons why obtaining umbrella insurance may be beneficial:

- Asset Protection: Umbrella insurance is designed to protect your assets, such as your home, vehicles, savings, and investments. In the event of a lawsuit or substantial claim, umbrella insurance can help cover costs that exceed the limits of your underlying insurance policies, providing you with financial security.

- Liability Coverage: Umbrella insurance offers liability coverage that extends beyond the coverage limits of your primary policies, such as auto or homeowners insurance. This means that if you are held responsible for an accident or injury, umbrella insurance can help cover legal expenses, medical bills, and other costs associated with liability claims.

- Comprehensive Protection: Umbrella insurance provides broad protection against various risks and liabilities. It can cover a wide range of incidents, including property damage, bodily injury, defamation, libel, slander, and even certain personal injury claims.

To determine if umbrella insurance is right for you, it is recommended to consult with your agent at Bear River Mutual. They have the expertise to assess your specific needs, evaluate your risk exposure, and help you make an informed decision.

Your agent will take into account your assets, lifestyle, potential liabilities, and budget to determine if umbrella insurance is a suitable option for you. They can provide personalized advice and guidance to ensure you have the appropriate level of coverage to protect your assets and provide peace of mind.

Reach out to your Bear River Mutual agent to discuss the benefits of umbrella insurance and determine if it is the right choice for your insurance portfolio. They are here to assist you in making informed decisions and securing the protection you need.